America’s national debt just hit $39 trillion, and the interest payments alone are now north of $1 trillion a year. That’s more than the entire GDP of Mexico. And yet, the new Fed chair, Kevin Warsh, has a plan to make this problem disappear—not by fixing it, but by redefining it.

Warsh’s big idea? Stop counting the things that actually make your life more expensive. Beef prices? One-time blip. Rent hikes? Just the market working. Oil shocks? Not real inflation. If this sounds like a sleight of hand, that’s because it is. And if it works, it won’t just change how we measure inflation—it’ll change who pays for America’s debt crisis.

The Beef With Beef: Why Warsh Thinks Your Grocery Bill Doesn’t Count

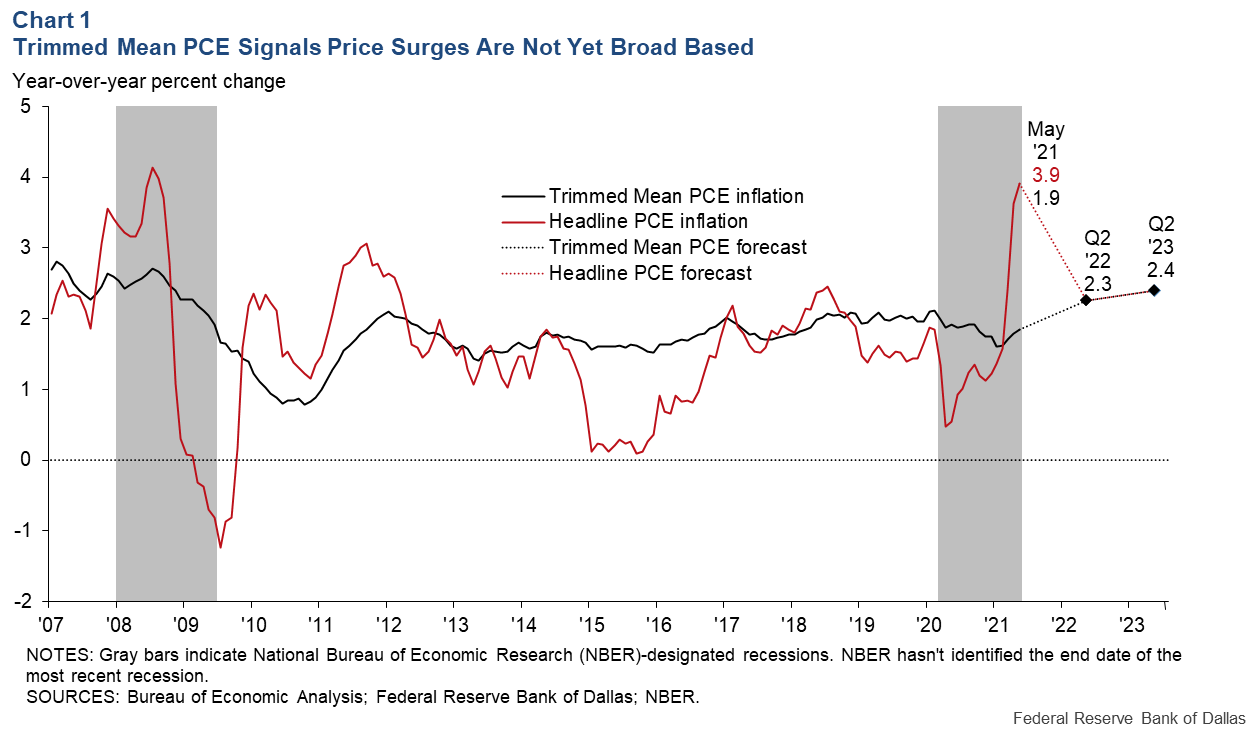

Warsh’s confirmation hearing was a masterclass in monetary gaslighting. His proposal? Ditch the traditional "core PCE" measure (which already excludes food and energy) and replace it with a "trimmed mean" approach. This method chops off the most volatile price changes—like, say, the cost of beef after a cattle shortage—and only counts the stuff in the middle.

The Dallas Fed already tracks this. In March 2024, while core PCE clocked in at 3.4%, the trimmed mean version was a cool 2.4%. That’s not a rounding error—that’s a full percentage point difference. And it’s the kind of number that lets the Fed declare victory over inflation while your rent still goes up 8% a year.

Warsh isn’t trying to solve inflation. He’s trying to solve the perception of inflation—so the Fed can cut rates without looking like it’s surrendering.

His logic isn’t totally insane. Milton Friedman, Warsh’s intellectual hero, argued that inflation is always a monetary phenomenon. If the money supply grows faster than the economy, prices rise. If not, price spikes are just temporary noise. But here’s the catch: Warsh’s trimmed mean method underestimated inflation during the 2021-2023 surge. It was the slowest measure to acknowledge the problem—and now he wants to use it to define the problem away.

The $39 Trillion Magic Trick: How Inflation Erases Debt

Here’s where it gets ugly. If Warsh’s method becomes the Fed’s North Star, it could justify rate cuts even if actual inflation is still running hot. And when interest rates fall below inflation, something magical happens to debt: it shrinks in real terms.

Imagine borrowing $100 to buy a monitor, and a year later, inflation has pushed the price to $120. You pay back $102, but that $102 buys less than it did when you borrowed it. The lender loses. You win. Now scale that up to $39 trillion.

This isn’t a conspiracy theory—it’s basic math. And it’s how countries have historically dealt with unsustainable debt. The U.S. did it after World War II. Latin America did it in the 1980s. The only difference? This time, the Fed might help it happen by pretending inflation is lower than it is.

America’s debt crisis isn’t going away. It’s just getting transferred—from the government’s balance sheet to yours.