The YouTube algorithm is serving up a new flavor of financial doom: "The UNTHINKABLE is About to Happen to Stocks." The video’s premise? That the Fed’s rate cuts—supposedly the market’s get-out-of-jail-free card—could actually trigger a sell-off worse than 2022. And the scariest part? The investors most at risk are the ones who think they’re playing it safe: retirees piling into "bulletproof" ETFs like SCHD, HNDL, and BND.

I’ll admit, my first reaction was eye-roll. Another day, another apocalyptic market take. But then I dug into the data—and the silence from the usual suspects. No one’s asking the hard question: What if this time, the Fed’s cuts don’t work? Not "won’t work perfectly," but won’t work at all. That’s the unthinkable scenario retirement ETFs aren’t priced for.

The Fed’s Rate Cuts Have a Dirty Secret

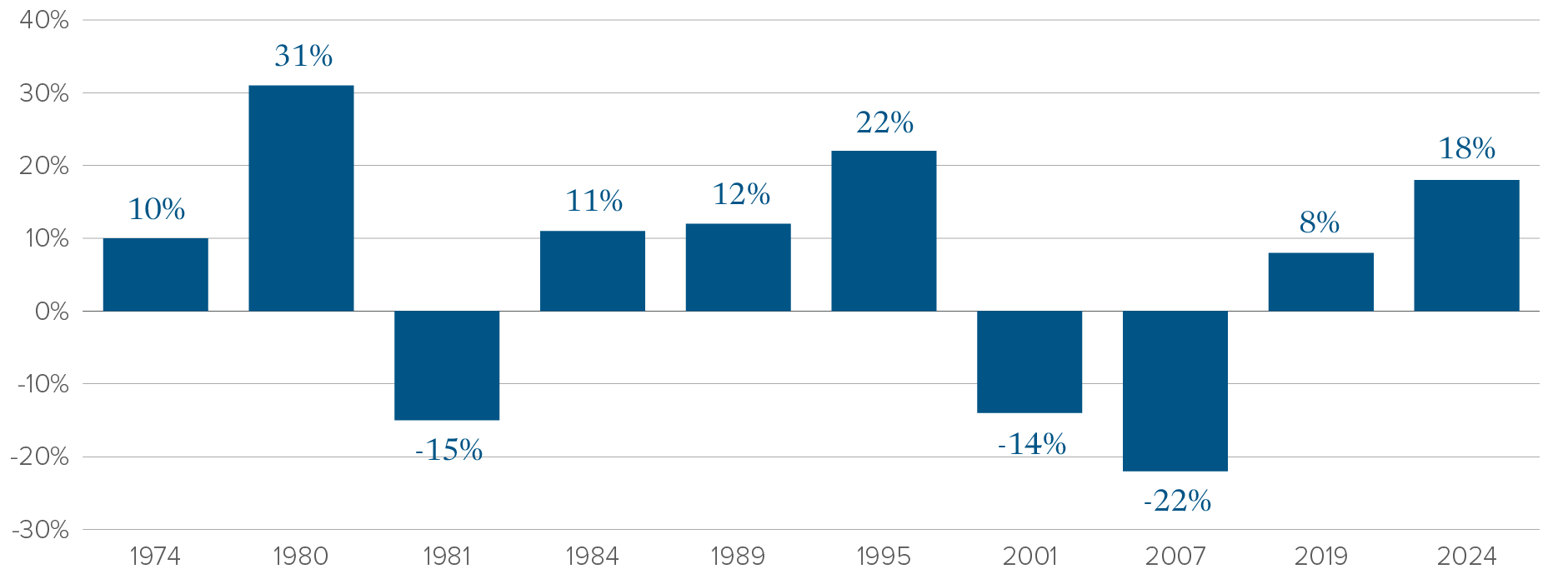

Conventional wisdom says Fed rate cuts = good for stocks. The playbook is simple: lower rates, cheaper borrowing, higher valuations. Rinse and repeat. But here’s the catch: it doesn’t always work that way. Since 1980, the S&P 500 has averaged a 9% return in the 12 months following the first rate cut of a cycle. Sounds great, right? Until you realize that average is dragged up by a handful of blowout years—like 2001 (+24%) and 2008 (+37%). The median return? A far less exciting 5%. And in 1981 and 2000? The market fell 10% and 13%, respectively, after the first cut.

The problem isn’t the cuts themselves—it’s what they signal. When the Fed cuts rates, it’s often because something is already broken. Inflation, unemployment, growth—pick your poison. And if the economy is weaker than expected, even cheap money can’t force corporations to grow earnings. That’s when the market’s multiple expansion party ends, and the fundamentals take over. For retirement ETFs built on the assumption of steady dividends and low volatility, that’s a problem.

Retirement ETFs Are Betting on a Goldilocks Economy

Retirement ETFs like HNDL and BND are designed to be the ultimate "set it and forget it" solutions. HNDL promises a 7% annualized distribution yield, while BND offers ballast against equity volatility. Both assume that the Fed will thread the needle—cooling inflation without killing growth. But what if they can’t?

Here’s the reality: the 10-year Treasury yield is sitting at 4.13%, and the Fed Funds Rate is at 3.75%. That’s a razor-thin margin for error. If inflation re-accelerates, the Fed could be forced to pause cuts—or even hike again. If growth slows too fast, corporate earnings could crater. Either way, retirement ETFs that rely on steady income and low volatility are suddenly exposed to the one thing they’re supposed to avoid: sequence-of-returns risk.

The Unthinkable Isn’t Priced In

The scariest part of the "unthinkable" scenario isn’t that it’s likely—it’s that it’s not priced in. Retirement ETFs are trading like the Fed’s cuts will be a smooth glide path to a soft landing. But history says otherwise. In 2000, the S&P 500 peaked after the first rate cut. In 2007, it took six months for the market to bottom. And in 2020? The Fed’s emergency cuts came after the COVID crash, not before.

The lesson? Rate cuts aren’t a panacea. They’re a signal that the Fed is playing catch-up. And if the economy is already weakening, even cheap money can’t force corporations to grow earnings. For retirement ETFs built on the assumption of steady dividends and low volatility, that’s a recipe for disappointment.